Donation tax system for municipal and metropolitan inhabitant taxes (hometown tax)

Updated: December 9, 2019

If you make a donation to a prefecture, city, ward, town, village, etc. that pays personal residence tax (prefectural tax/municipal tax), the amount exceeding 2,000 yen of the donation will be deducted from personal residence tax (local tax). ) and donations can be deducted from income tax (national tax).

Note 1 = You can freely choose the prefecture/city/ward/town/village where you make your donation (donations that are eligible for deduction do not need to be in your hometown city/ward/town/village).

Note 2: Regarding donations related to the Great East Japan Earthquake, if donations are made to local governments via fundraising organizations (Japanese Red Cross Society, etc.), they will be treated as "hometown donations."

About I (Ai) Town Inagi Support Donation (Hometown Tax)

Click here if you are considering donating to Inagi City.

Target date

Notes on donations paid from January 1st to December 31st of each year: Personal residence tax will be deducted from the personal residence tax for the year following the donation, and income tax will be deducted from the income tax for the year the donation was made.

Eligible donations

In addition to the conventional local governments (prefectures, cities, wards, towns and villages), prefectural community chest of the place of residence, Japanese Red Cross Society branch of the place of residence, donations to corporations etc. designated by local governments by ordinance.

overview

1 Deductible limit for donations (limit amount to which donation deduction applies)

30% of total income, etc.

2 Applicable minimum amount (minimum amount to which donation deduction will be applied)

2,000 yen per year

Basic deduction amount

(Donation amount - 2,000 yen) x 10%

Note: 10% is 6% municipal tax and 4% metropolitan tax.

Hometown tax special deduction

For donations to local governments (prefectures, cities, wards, towns and villages), the special deduction amount is further deducted from tax.

| (1) Basic deduction amount | (donation amount -2,000 yen) x 10% |

|---|---|

| (2) Exceptional deduction amount | The lesser of the following A or B |

| Donation deduction amount | (1)+(2) |

Note 1=The marginal income tax rate is the highest rate of income tax applicable to the person. From 5% to 45% depending on taxable income.

Remark 2 = Only the basic deduction amount is available for donations to organizations other than local governments.

Note: Please refer to the following for deductions for donations specified in the ordinance.

Remark 3 = If the deduction for donations is applied, the special income tax for reconstruction will also be reflected, so the special deduction for hometown donations on municipal and metropolitan inhabitant taxes will be adjusted.

Donations specified by ordinance

A system has been established that allows prefectures, municipalities, and municipalities to add donations designated by ordinance to individual residence tax deductions from among donations eligible for income tax deduction.

Donations subject to deduction

Among donations eligible for income tax deduction, certain corporations that have a business or office in the city

Note: Among donations eligible for income tax deduction, certain corporations within the city are social welfare corporations and school corporations (other than certain corporations eligible for donation deduction specified by the ordinance are national university corporations and certified NPO corporations). etc., but there are currently none in the city).

Note: The donation will be deducted from your personal municipal tax in the year following your donation.

Note: To confirm whether the recipient of your donation is a corporation eligible for tax deduction, please contact the recipient or the municipal tax section of your city hall.

Deduction Amount

The amount obtained by subtracting 2,000 yen from the donation amount and multiplying it by 6% will be deducted from your personal municipal tax.

Note: If the donation falls under the category of deductible donations designated by the Tokyo Metropolitan Government, it will also be deducted from personal inhabitant tax (the amount calculated by subtracting 2,000 yen from the donation amount and multiplying it by 4%). .

Please check the "Ministry of Internal Affairs and Communications hometown tax portal site" for an estimate of the amount of hometown tax to be deducted in full (excluding 2,000 yen).

![]() Ministry of Internal Affairs and Communications Hometown Tax Portal Site (External link)

Ministry of Internal Affairs and Communications Hometown Tax Portal Site (External link)

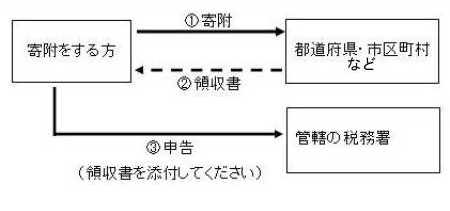

How to report (receipt issued by the donation destination is required for reporting)

Those who declare donation deduction for income tax and individual inhabitant tax

Please file a final tax return at the tax office in the jurisdiction of your residence.

Note: Please also refer to this site.

![]() Income tax return preparation corner (external site)

Income tax return preparation corner (external site)

Those who are not subject to income tax and only declare deductions for taxable individual inhabitant tax

Please report to the municipality where you live on January 1st of the year following the donation.

Flow of donation deduction

Note: Be sure to keep your receipt as you will need it when filing your tax return.

When using the hometown tax one-stop service (applies to donations made after April 1, 2015)

The one-stop special system is a system that allows salaried workers who do not need to file a final tax return to receive tax credits for donations without filing a final tax return under certain conditions.

This system can be applied to hometown donations made after April 1, 2015 by applying to the local government to which the donation is made. If the one-stop exception system is applied, there will be no deduction for income tax, and municipal and metropolitan inhabitant taxes for the following fiscal year will be reduced. If there is a change in the application form, such as a change of address, after applying for the exception, it is necessary to submit a change notification form to the local government to which the donation is made by January 10 of the year following the hometown tax payment.

(Note) Those who paid hometown tax between January 1, 2015 and March 31, 2015 must file a tax return.

Those who are not eligible for the one-stop exception system

Please note that those who meet the following criteria are not eligible for the one-stop exception system.

- Those who need to file an income tax return or municipal/prefectural inhabitant tax return for purposes other than receiving donation deductions for the hometown tax payment.

- Those who file income tax returns

- Those who file municipal and metropolitan inhabitant tax returns

- Those who donate to more than 5 organizations